NBP Saibaan is a product offered by National Bank of Pakistan under Mera Pakistan Mera Ghar scheme. Like many others banks NBP Saibaan is offered under the PM’s Naya Pakistan Housing Scheme.

NBP Saibaan will offer an opportunity to fullfil the dream of owning a house. Under this scheme applicants can purchase a home, have it constructed or purchase a land and construct a home on cheaper rates.

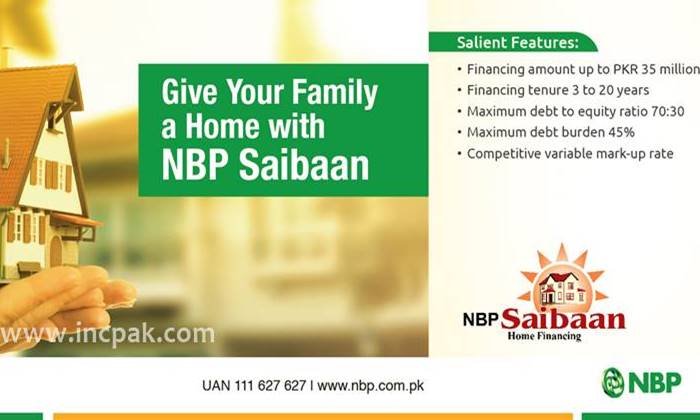

The offered under NBP Saibaan is up to 35 Millions, the financing period of which is 3 to 20 years.

The loan facility is available for all Pakistani nationals with satisfactory credit history. The income requirement for government is as low as Rs.5000/-.

For other salaried Class minimum net take home salary requirement is Rs. 10,000/-. For Business Persons & Self-Employed Professionals minimum net take home is PKR 15,000/-.

Products Offered Under NBP Saibaan

1. Home Purchase (House or Apartment)

| Financing Amount | Upto 35 Million |

| Financing Period | 3 to 20 years |

| Debt and Equity | 70:30 (Maximum) |

| Debt Burden | 45% (Maximum) |

2. Home Construction

| Financing Amount | Upto 35 Million |

| Financing Period | 3 to 20 years |

| Debt and Equity | 70:30 (Maximum) |

| Debt Burden | 45% (Maximum) |

3. Land Purchase Plus Construction

| Financing Amount | Upto 35 Million |

| Financing Period | 3 to 20 years |

| Debt and Equity | 70:30 (Maximum) |

| Debt Burden | 45% (Maximum) |

4. Balance Transfer Facility (BTF)

(If you have a Home Finance Facility outstanding with another bank you can have it transferred to NBP.

General Information

The markup rate being offered is Variable. The variable markup rate is pegged with SBP Discount Rate with spread of 2% in which Life & Disability Insurance coverage is mandatory. The markup rate is revised on every financing anniversary if there is change in SBP Discount Rate. Bank has the right to change the spread for fresh cases.

The mode of repayment is direct deduction (through debt authority) of Installment from salary account or the Customer’s Current Account at NBP which has to be kept funded with at least one monthly installment amount.

Repayment is monthly in the form of Total Monthly Installment (TMI) comprising of principal, mark-up, insurances portions according to the amortization schedule based on pricing and tenure. The amortization schedule will be revised if there is change in bench marked rate on financing anniversary after every 12 installments.

Property insurance and life & disability insurance coverage is mandatory.

Fees, charges and government taxes apply.

Full or partial (balloon) within 5 years will be subjected to early payment service charges @ 2 % of the amount being paid, after 5 years no charges will apply.

In case of late payment, returned cheques and delay in construction, service charges will be levied as per NBP’s approved tariff.

*NBP conditions apply

Eligibility Criteria

Eligibility *

- Must be Pakistani resident national, having satisfactory credit history.

- Salaried Class, Self-Employed Professionals and Business Persons.

- Property being financed is to be located in NBP approved localities.

Age Requirement:

- For Salaried Class the minimum age is 22 years at the time of applying for the financing facility and the financing facility should expire at maximum age of 59.5 years.

- Similarly for Business Persons and Self-Employed Professionals minimum age is 21 years at the time of applying for the financing facility and maximum age should not be more than 65 years at the time of the maturity of the finance.

Income Requirement:

- For Govt. employees it is PKR 5000/- whose monthly salary is directly credited to his/her account maintained with NBP and employer undertaking is provided.

- For rest of Salaried Class minimum net take home is PKR 10,000/-.

- For Business Persons & Self-Employed Professionals minimum net take home is PKR 15,000/-.

Length of Service/Business Requirement:

- Minimum 2 years with the same employer or otherwise collective and continuous employment of 3 years.

- For Business Persons & Self-Employed Professionals a minimum past history of 3 years relationship with business.

* NBP conditions apply

Required Documents

With duly filled Applications Form:*

- Two attested passport size photographs.

- Two attested copies of your CNIC.

- Two attested copies of CNIC of references.

- Cheque for the processing charges.

- Cheque in favor of legal counsel for legal opinion.

- Cheque in favor of Valuator for valuation report.

- Cheque in favor of Income Estimation Company for income estimation report, if applicable.

- Property Documents: Attested copy of title documents available (other documents may be required).

- Bill of Quantity (BOQ) in case of HC and LPC.

1) FOR SALARIED PERSONS, WHOSE SALARIES ARE DISBURSED THROUGH NBP BRANCH

- Employer undertaking for remittance of salary at relevant NBP Branch for credit to salary account (to be provided at a later stage, format available at relevant Branch).

- Salary Certificate/Service Certificate.

- Copy of employee ID attested by NBP Branch (where applicable).

- Attested copies of last three (3) months salary slips.

- Attested copies of last three (3) months bank statement.

2) FOR SALARIED PERSONS OF MNCs AND NBP APPROVED COMPANIES

- Employer undertaking duly attested by relevant NBP Branch, where applicable

- Letter of Verification of Employment on Company Letterhead mentioning the date of joining.

- Salary Certificate/Service Certificate.

- Copy of employee ID attested by NBP Branch.

- Attested copies of last three (3) months Salary Slips.

- Attested copies of last three (3) months bank statements

3) FOR OTHER SALARIED PERSONS

- Letter of Verification of Employment on Company Letterhead mentioning the date of joining.

- Salary Certificate/Service Certificate.

- Attested copies of last three (3) months Salary Slips

- Attested copies of last twelve (12) months bank statements

- Attested copies of last three (3) months paid bills for electricity and telephone OR copies of last (12) twelve months credit card bills (whichever is available).

4) FOR BUSINESS PERSONS

- Bank Certificate stating applicant maintaining Business Account and the date of account opening.

- Attested copy of latest Form 29 in case of Private or Public Limited Company.

- Attested copy of Partnership Deed (where applicable)

5) FOR SELF-EMPLOYED PROFESSIONALS

- Attested copy of current professional association membership/practicing certificate.

- Adequate proof of professional engagement like bank certificates.

- Attested copy of Partnership Deed (where applicable)

**Any other document may be required on case to case basis by the bank.

How to Apply

Instructions for completing the Application Form:

- Fill-in the form completely

- Print the “completely filled” form

- Get it signed by Referees

- Sign it yourself

- Attach the Required Documents

- and submit “In PERSON” to NBP Saibaan Team **

Note: The form is designed to be viewed in Adobe Acrobat Reader

NBP Saibaan Application Form

** Applicant should submit the Form himself (in-person/ by hand) to NBP Saibaan Team with a non-refundable fees of Rs. 15.Now, housing for all* with NBP Saibaan* NBP conditions apply

Frequently Asked Questions

Q-1. What is NBP Saibaan?

A-1. NBP Saibaan is a Housing Finance Product

Q-2. Who are eligible for NBP Saibaan?

A-2. All Pakistani resident nationals, CNIC Holder, having clean eCIB & DataCheck reports and maintaining salary / current account with NBP subject to fulfillment of the policy parameters of NBP Saibaan.

Q-2. What kind of Products are offered under NBP Saibaan?

A-2. Following five products are being offered under NBP Saibaan:

- Home Purchase Finance (HP), for the purchase of ready residential house or apartment.

- Home Construction Finance (HC), for construction and extension of self owned residential property.

- Balance Transfer Facility (BTF), for taking over house loan from other financial institute.

- Land Purchase plus Construction (LPC), for purchasing of residential plot and subsequently.

Q-3. What is Balance Transfer facility (BTF)?

A-3. If a customer has already availed housing finance facility from another bank then his/her outstanding financing amount can be transferred to NBP subject to a 24 months satisfactory repayment history and fulfillment of all the terms and conditions of NBP Saibaan.

Q-4. What is the maximum financing amount being offered under NBP Saibaan?

A-4. Maximum financing amount being offered is as under:

Home Purchase PKR Up to 35 million

Home Construction PKR Up to 35 million

BTF PKR Up to 35 million

Purchase of Land plus construction PKR Up to 35 million

(Financing amount shall depend upon the net take home salary/income of the borrower and other product criteria).

Q-5. What is the tenure of the financing?

A-5. The tenure for products is as under:

- Home Purchase 3 years to 20 years

- Home Construction 3 years to 20 years

- BTF 3 years to 20 years

- Purchase of Land plus construction 3 years to 20 years

(Actual tenure depends on age of the customer).

Q-6. What is the Debt to equity ratio?

A-6. Product wise debt to equity ratio is as under:

- Home Purchase 70:30

- Home Construction 70:30

- BTF 70:30

- Purchase of Land plus construction 70:30

Q-7. What is the maximum percentage allowed for debt burden?

A-7. The maximum debt burden percentage is 45%.

Q-8. What type of mark-up rate is being offered and what is the bench markup of mark-up rate?

A-8. The markup rate being offered is Variable. The variable markup rate is pegged with SBP Discount Rate with spread of 2% in which Life & Disability Insurance coverage is mandatory. The markup rate is revised on every financing anniversary if there is change in SBP Discount Rate. Bank has the right to change the spread for fresh cases.

Q-9. Is Grace Period available under NBP Saibaan?

A-9. Maximum grace period allowed in Home Construction and Land Purchase plus Construction cases is 15 months. During this grace period the monthly installment comprises of markup and insurance amount only. No grace period is allowed for Home Purchase, Home Improvement and BTF.

Q-10.What is the minimum income requirement?

A-10. The minimum income requirement is as under:

- For Govt. employees it is PKR 5000/- whose monthly salary is directly credited to his/her account maintained with NBP and employer undertaking is provided.

- For rest of Salaried Class minimum net take home is PKR 10,000/-.

- For Business Persons & Self-Employed Professionals minimum net take home is PKR 15,000/-.

Q-11. What is the minimum & maximum age requirement?

A-11. Details are as under:

- For Salaried Class the minimum age is 22 years at the time of applying for the financing facility and the financing facility should expire at maximum age of 59.5 years.

- Similarly for Business Persons and Self-Employed Professionals minimum age is 21 years at the time of applying for the financing facility and maximum age should not be more than 65 years at the time of the maturity of the finance.

Q-12. What is the mode of repayment?

A-12. The mode of repayment is direct deduction (through debt authority) of Installment from salary account or the Customer’s Current Account at NBP which has to be kept funded with at least one monthly installment amount.

Q-13. Can NBP Saibaan be applied with Co-applicant?

A-13. Yes, NBP Saibaan can also be applied with Co-applicant. Spouse, parents and adult male children can be co-applicant. Co-applicant’s income may be clubbed.

Q-14. What will be processing fees and External Agencies charges?

A-14. Details are as under:

For Govt. employees PKR 500/- irrespective of the finance amount.

For others

PKR 1000/- for financing up to PKR 1 Million

PKR 3000/- for financing up to PKR 4 Million

PKR 6000/- for financing above PKR 4 Million.

Income estimation, legal and valuation fee will be charged as per actual, which varies from Region to Region.

Q-15. What is length of service/business requirements?

A-15. The requirement of length of service/business is as under:

- Minimum 2 years with the same employer or otherwise collective and continuous employment of 3 years.

- For Business Persons & Self-Employed Professionals a minimum past history of 3 years relationship with business.

Q-16.What is the property eligibility criteria?

A-16. Property eligibility criteria is as under:

- Property should be located in “positive areas” as defined by the Bank.

- Property should be purely residential and for self-occupancy.

- For Home Purchase finance, property should be an already constructed house or apartment.

- Title of property shall be clear and chain of documents should be complete.

- Satisfactory valuation and legal opinions from the Bank designated valuators and lawyers are to be required on each property.

Q-17. What is the Property and Life & Disability Insurance requirements?

A-17. Both property and life & disability insurance coverage is mandatory. The premium rates are as under:

- For property insurance, the premium rate is 0.1% of 120% of approved finance amount. The premium of first year insurance is paid in advance and for subsequent years it is part of the monthly installment amount.

- For life and disability insurance, the standard premium rate is 0.525%** of approved finance amount. The premium of first year insurance is paid in advance and for subsequent years it is part of the monthly installment amount.

- All insurance charges shall be borne by the customer.

**Rates could vary depending upon the assessment of actual risk based on medical examination of the borrower by the Insurance Company. Moreover, if due to medical reason the coverage is declined then financing request is also declined.

Q-18. What is the collateral requirements?

A-18. The requirements of collateral are as under:

For collateral purposes, the property for the purchase/construction/BTF and LPC for which the financing is being provided, will be mortgaged.

Equitable and partly Registered Mortgage will be created on the property. Cost of the same to be borne by the customer. However, Bank may require 100% registered mortgage.

All the original property documents will be in Bank’s custody.

Q-19. How disbursement will be made?

A-19. Details are as under:

- In Home Purchase, Home Improvement and BTF, the disbursement is made in one go.

- In Home Construction, the disbursement is made in maximum of 4 tranches.

- In Land Purchase plus Construction, the disbursement is made in maximum of 5 tranches.

** Rates/Charges are subject to change as per market factor/SBP regulations etc.

For more information, contact the nearest designated NBP Branch

Also Check the Mera Pakistan Mera Ghar ‘Naya Pakistan Housing Scheme’ Loan facility by other banks

{kind=link}